India’s Unified Payments Interface (UPI) has transformed how millions handle digital transactions, offering instant and free money transfers that span banks and payment apps. However, the Reserve Bank of India (RBI) has warned that this popular, no-cost model may not be viable forever. Policymakers are now questioning who will pay the mounting costs as digital payments soar, and hint that some charges might become inevitable in the future.

UPI’s Explosive Growth and the Burden of Zero Charges:

Over the past two years, UPI’s daily transactions more than doubled-from 310 million (31 crore) to over 600 million (60 crore) a day. This explosive usage underscores the platform’s success, but it also means enormous operational and technological costs are being absorbed by banks, payment providers, and the National Payments Corporation of India (NPCI). Currently, there is no direct revenue stream from UPI transactions for these actors, as the government mandates a zero merchant discount rate (MDR), effectively making all payments free for users and merchants.

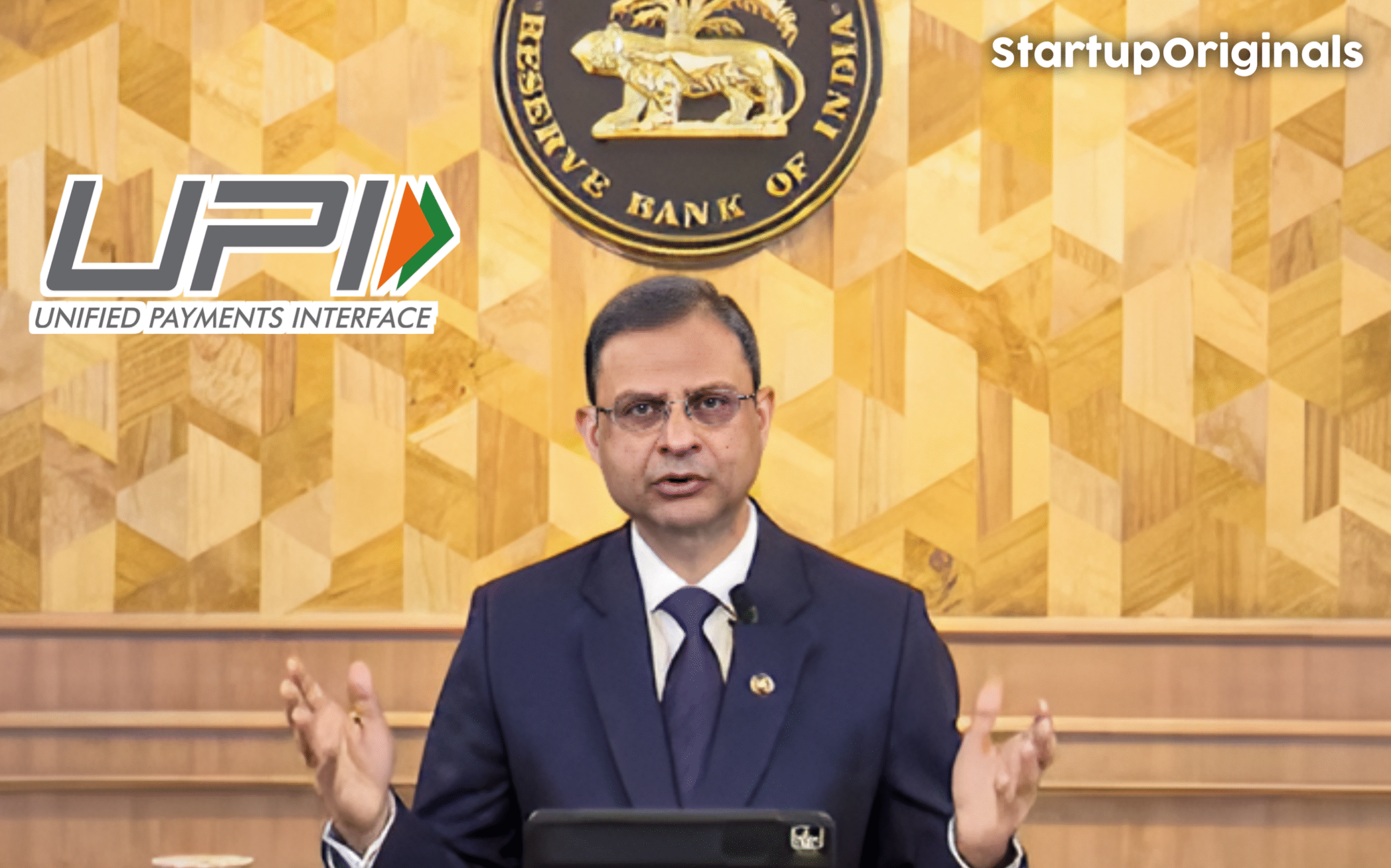

RBI’s Chief Flags Urgent Sustainability Concerns:

RBI Governor Sanjay Malhotra has made it clear: while digital payments promote convenience and financial inclusion, the “free for all” setup is not financially sustainable in the long run. At a recent media event, Malhotra explained that the government is currently subsidizing the UPI infrastructure, supporting banks and stakeholders to keep the system running smoothly. “Payments and money are a lifeline… As of now, there are no charges. But obviously, some costs have to be paid,” he stated, signaling that the government cannot continue this subsidy forever.

Who Will Pay? The Debate Over UPI Charges:

The central issue revolves around whether and how users or merchants should pay for UPI in the future:

- Banks and fintechs have repeatedly pushed for a modest MDR, especially for high-value transactions or large merchants, saying the zero-charge model is becoming unmanageable as technical and infrastructural costs mount.

- The government, on the other hand, has insisted on keeping UPI free for end-users and merchants for now, calling it a “digital public good.” Instead of charging, it subsidizes participants and offers special incentives as compensation.

- Public sentiment remains strongly against paying for UPI. Surveys suggest most users would cut down or stop using UPI if any transaction charges are introduced.

What Could Happen Next?

Governor Malhotra hinted at coming changes, stressing that “any important infrastructure must bear fruits, and its cost should be paid-whether collectively or by the user”. The RBI and government face a tough choice:

- Reinstate or introduce a small MDR for certain transactions, likely on high-value or business payments.

- Continue subsidies or introduce a “shared cost” model.

- Ensure that robust, secure, and accessible digital payments remain a central feature of India’s financial ecosystem, even as costs rise.

Wider Economic Context: Policy & Inflation

At the same event, the RBI Governor also addressed the nation’s monetary policy outlook:

- Interest Rates: The RBI maintains a neutral stance and may lower rates further if inflation remains low. Malhotra emphasized flexibility based on how inflation and economic growth evolve. India’s current inflation is at 2.1%, well below the upper target of 6%, but may rise to 4.4% for the January–March quarter.

- Credit Growth: Previous rate cuts have already led to cheaper new loans, supporting lending and economic activity, even as overall credit growth has been moderate.

The Way Forward for UPI:

While UPI remains a cornerstone of India’s digital economy, its future funding cannot rely on government subsidies alone. The RBI’s warning is a wake-up call that new policies are needed to ensure this critical infrastructure grows sustainably, protecting both innovation and end-user access.